Most retail investors in India discovered SGX Nifty the hard way — after a session where their positions moved in a direction they did not expect and someone explained, after the fact, that the offshore futures had been signalling that move for hours. That kind of education tends to stick. And once traders understand what SGX Nifty actually does, they rarely stop tracking it.

The Offshore Futures Contract That Watches India From Abroad

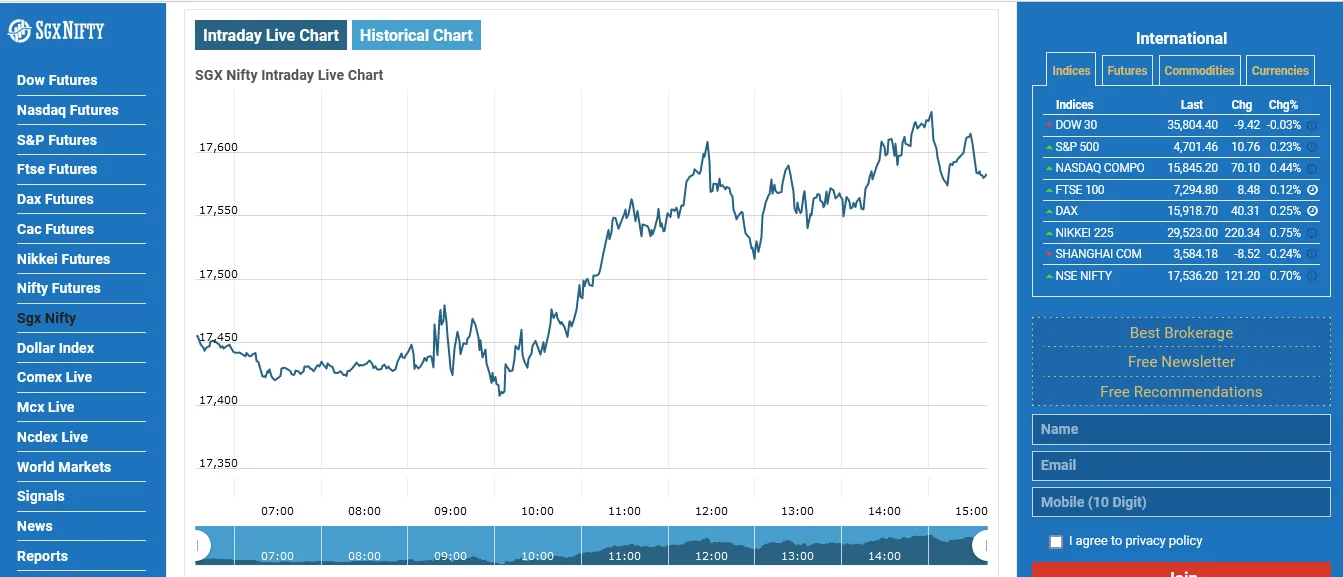

With the SGX Nifty futures contract, which is based on the Nifty 50 index that was traded on the Singapore Exchange, foreign buyers can invest in Indian stock markets without being limited by local trading hours or the rules that apply to NSE players.

The significance of this is straightforward. Global capital does not stop moving because Indian exchanges are closed. Hedge funds in New York, asset managers in London, and proprietary desks across Southeast Asia continue adjusting their exposure to Indian equities based on whatever is happening in their own time zones. SGX Nifty was the instrument through which that adjustment happened — visibly, in real time, with actual money behind every price move.

Why Institutional Investors Paid Close Attention

The connection between SGX Nifty and the domestic Nifty runs through institutional behaviour rather than any direct mechanical linkage. Foreign institutional investors frequently used the Singapore-listed contract to hedge existing Indian equity positions or build new ones ahead of anticipated domestic moves.

When large FII positions shifted significantly in the offshore contract, it created a directional bias that domestic participants had to account for. Ignoring SGX Nifty movements was not really an option for anyone managing serious capital — the two markets were too interconnected for that kind of selective attention.

Over time, even mid-sized domestic traders began incorporating the offshore signal into their broader view, not as a rule but as a data point that carried weight when everything else was ambiguous.

Where SGX Nifty Diverged From Domestic Reality

The more instructive relationship between SGX Nifty and the Nifty is not when they moved together — it is when they did not. Global sentiment and domestic fundamentals are different animals. A strong overnight read on the offshore contract built on U.S. equity momentum meant very little on days when RBI surprised markets, when quarterly earnings from index heavyweights disappointed, or when rupee depreciation spooked domestic institutions into selling.

Experienced traders learned to treat divergence between SGX Nifty levels and actual Nifty behaviour as a signal in itself. When domestic markets refused to follow a bullish offshore lead, it usually meant that something local was exerting pressure that global participants had not priced in yet.

The Transition and What It Changed

SGX Nifty was eventually succeeded by GIFT Nifty in 2023, shifting the offshore Nifty futures activity under a structure more closely aligned with Indian regulatory frameworks. The instrument changed. The underlying logic — that global money needs a way to express views on Indian equities outside domestic trading sessions — did not.

Understanding SGX Nifty remains relevant for any trader studying how Indian markets have historically responded to international capital flows, and why the gap between global sentiment and domestic price action has always been one of the most exploitable inefficiencies in Indian equity trading.