In the middle of the pandemic, Indians learnt new lessons about health and wealth. It was not just building physical immunity that was key, but also financial immunity.

Getting vaccinated against COVID-19, increasing the protection coverage through insurance, cutting down on discretionary spending, accumulating emergency funds etc. These are just some of the steps that Indians took to become economically secure and boost financial immunity.

SBI Life Insurance conducted its Financial Immunity Survey 2.0 to understand these trends better. Here, 57% of the survey respondents associated financial immunity with maintaining financial security for self and family. 78% of Indians feel that Insurance is an extremely important part of financial planning.

The survey showed that Indians are utilizing half of their income to build financial immunity through savings, investments, and insurance.

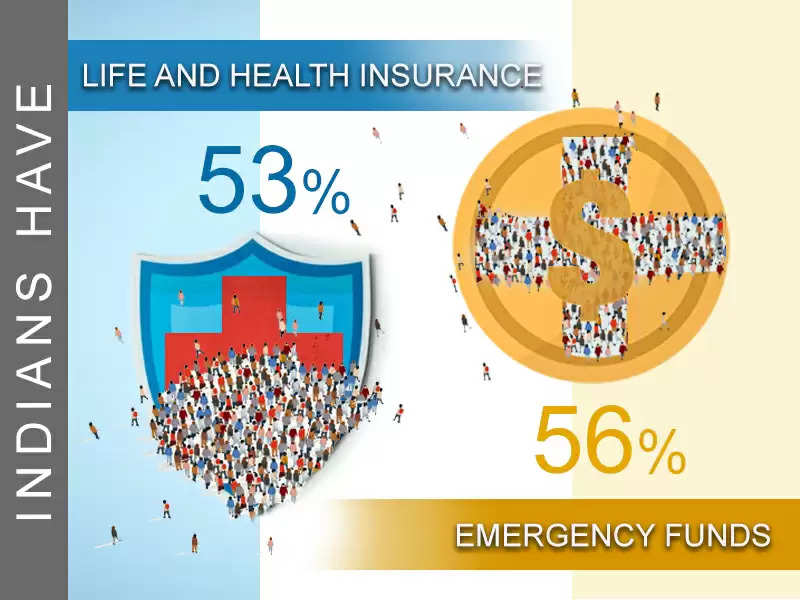

According to the survey, 56% of Indians have accumulated emergency funds since the pandemic and 53% have insured themselves with life and health insurance.

In addition, three out of four Indians have increased their savings since January 2021. Of this, 56% of the Indians will use this accumulated amount to buy life insurance even as the third wave has hit.

The coronavirus outbreak was a major factor in this behavioural change. Millions fell sick, several lives were lost, and hospitalisations led to mounting bills. It was then that Indians realised for a secure future they needed to stay fit and build physical and financial immunity.

Due to the extended lockdown, job losses happened, pay cuts were initiated by companies and Indians needed to get their finances in order. Individuals who had already purchased insurance policies could cope better, since their policy claims covered the costs.

Financial immunity was not just building a reasonable corpus but also involved earning income from multiple sources. Building an adequate corpus to improve the finances involved insurance purchases, too.

Why insurance?

The pandemic impacted people’s ability to spend. SBI Life’s survey showed that 64% of the Indians felt an impact on their milestones previously set. This was an indicator that there was either an absence of financial preparedness or it was impacted due to the sudden crisis.

Unknown risks are a rising threat globally. Emergency medical care, accidents, or even diagnosis of critical illness would call for expensive treatment. Amidst this, the sudden death of an earning family member would have disastrous emotional and financial consequences for the dependents.

It is here that buying an insurance policy comes in handy. The earlier it is bought, the better it is for the family. For salaried professionals with dependent parents, spouses, and/or children, a protection plan that offers financial backing in case of death is a must-have. Realising the importance of insurance, 44% & 46% Indians bought Life and Health insurance respectively for the first time after March 2020, reveals the survey.

While it is important to have a diversified investment strategy, insurance needs to be the first part of this puzzle. Be it protection against financial uncertainties, planning for a child and their future, or even retirement, insurance policies cover up these expenses.

Even if there is the unfortunate death of a family member, it is life insurance that can ensure that the financial immunity stays intact. Rising inflation and a steep hike in the price of essential commodities mean that one must plan ahead for the future.

How many middle-class salaried professionals can save a crore in anticipation of financial uncertainties? But paying as low as Rs 7,000-8,000 for a Rs 1 crore term insurance plan is doable. This is how life insurance helps bridge the gap.

In addition, there are tax benefits for life insurance premium payments under Section 80C of the Income Tax Act. This further builds financial immunity.

Are you adequately insured?

Underinsurance or buying inadequate sizes of insurance covers is a concern in India. About 59% of SBI Life’s respondents said that they are worried about rising medical & treatment costs, instability of jobs and the health of themselves/their family.

Yes, some steps have been taken to curb expenses, including buying insurance and spending less on non-essential items. But is that enough?

It is essential to not just buy insurance but be adequately covered. Findings from SBI Life’s Financial Immunity Survey 2.0 found that Indians are under-insured with just ~3.8 times the cover of their annual income. The recommended level is 10-25 times the yearly income. And those who had adequate insurance have higher levels of financial immunity.

A regular financial assessment is necessary to plan for the related expenses for milestones such as marriage, childbirth, and retirement. The insurance cover should be large enough to pay for these requirements.

Life is unpredictable, and the ongoing Covid-19 has aggravated this situation. Buying the right insurance cover at the right time could help develop that much-needed financial immunity.

Disclaimer: This article has been produced on behalf of SBI Life by Mediawire team.